In March 2022, the National Private Lenders Association passed a formal resolution. The membership voted to stop using the term "hard money" — not informally, not as a preference, but as an official industry position. The preferred replacements: "private lending," "bridge lending," and "transitional lending."

It was a quiet vote with an interesting implication. The two terms most real estate investors use interchangeably — hard money and private money — were being collapsed into one by the very industry they describe. And the one surviving was private lending.

That context matters when someone searches "hard money vs. private money lending." The question assumes a clean distinction. The industry's answer, increasingly, is that the distinction is collapsing — and understanding why is more useful than memorizing the old definitions.

Where the Terms Come From

Hard money has a straightforward etymology. The loan is secured by a hard asset, meaning real property. The term emerged to distinguish asset-backed lending from soft loans — unsecured credit based on a borrower's promise to repay. Hard money lenders, by definition, cared less about who the borrower was and more about what they were buying.

Private money developed as a parallel category, describing capital that comes from private individuals rather than institutions. A friend with capital, a high-net-worth investor looking for yield, a family connection willing to lend on a deal — these were private money lenders. The relationship was the underwriting.

For a period, the distinction was meaningful. Hard money meant a professional company with a standardized process. Private money meant an individual with personal capital and flexible terms. The two categories operated differently and attracted different borrowers.

That period is largely over.

What Changed

The private lending industry matured significantly after 2008. As banks retreated from real estate investment lending under post-crisis regulatory pressure, private capital filled the gap at scale. What had been a fragmented collection of regional hard money shops and individual investors evolved into a more professionalized market: lending companies with institutional capital behind them, systematic underwriting processes, loan origination software, and compliance infrastructure.

The result was a category of lender that looked a lot like what people used to call hard money — professional, asset-based, fast-closing — but operated with the capital depth, reliability, and borrower-relationship orientation that used to be associated with the better end of private money. These lenders didn't call themselves hard money lenders. They called themselves private lenders.

At the same time, the "hard money" label had accumulated reputational baggage. It carried connotations of last-resort financing, predatory terms, and lenders whose strategy, as practitioners in the space describe it, was "lend to own" — structuring loans to profit from default rather than repayment. Whether or not that reputation was earned broadly, it had become a liability.

Both the AAPL and the NPLA made retiring the term a sustained focus through 2021 and 2022. The AAPL — originally founded as the National Hard Money Association in 2009 before changing its name — published "The Demise of 'Hard Money' in a Private Lending World" and had been pushing in this direction since its formation. The NPLA followed with its formal resolution in March 2022, according to Scotsman Guide. Both associations urged members to cease using the term on their websites, marketing materials, and communications.

The rebrand went beyond something cosmetic. It reflected something real about how the industry had changed.

The Distinction That Still Exists

Terminology aside, there are still meaningful differences between types of non-bank real estate lenders. The old hard money vs. private money frame just isn't the cleanest way to describe them.

The more useful distinction is between individual capital and institutional capital.

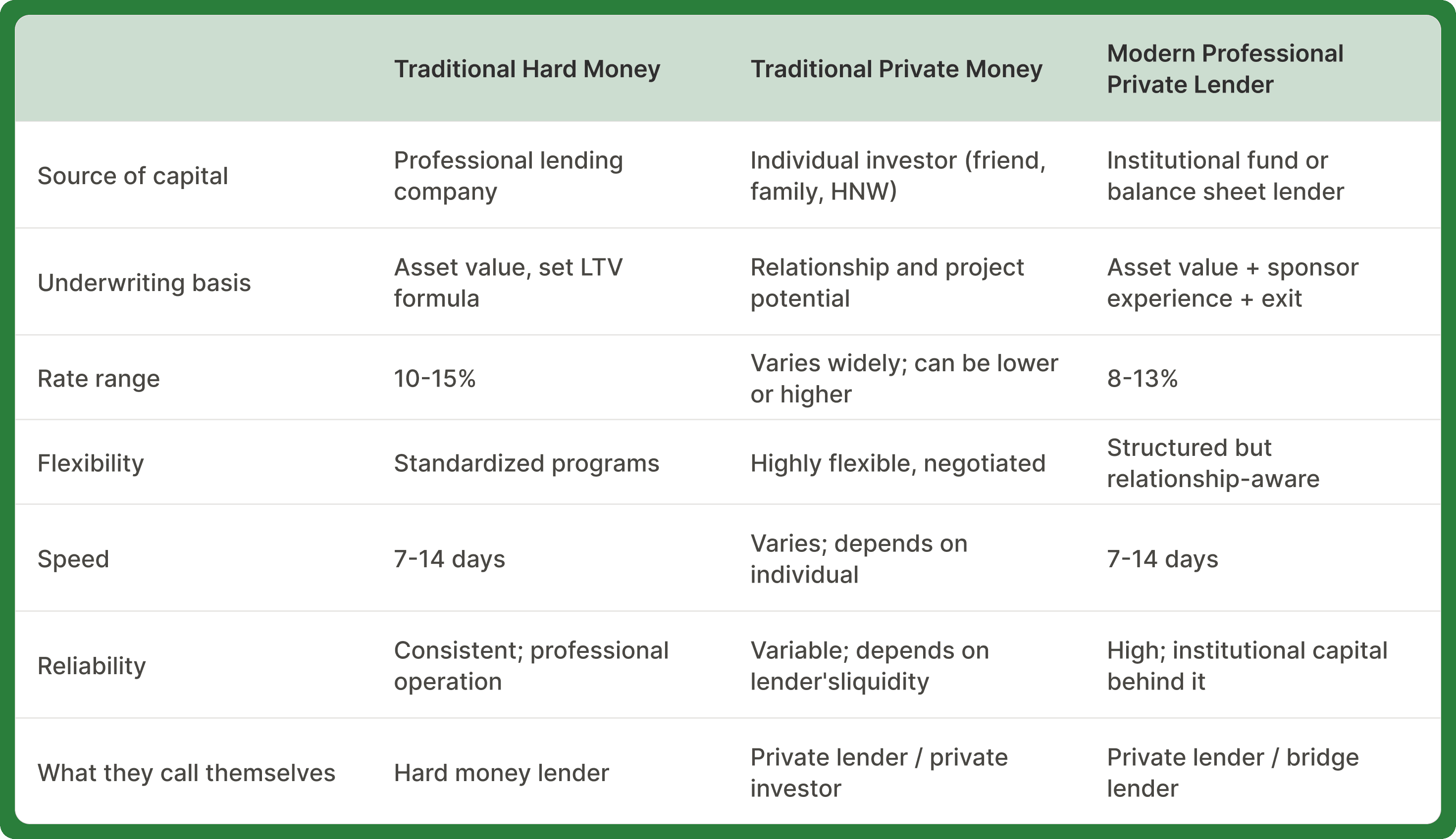

Individual capital lenders are exactly what the original private money definition described: people deploying their own money, usually on a relationship basis, with terms that reflect the flexibility and personal nature of the arrangement. Rates can be lower — or more variable. Terms can be more creative. A borrower with the right connection can access capital in ways a professional lender wouldn't offer. The tradeoff is reliability — individual lenders have finite capital, variable liquidity, and no institutional process behind them.

Institutional capital lenders are professional lending operations funded through debt funds, warehouse lines, or balance sheet capital. Their underwriting is systematic, their programs are defined, and their ability to close is backed by real capital depth. Rates are higher than what a well-connected borrower might negotiate with an individual, but the certainty of close is significantly stronger.

Much of what the market calls "private lending" today falls in the institutional category. Much of what was historically called "hard money" also falls there now. The two labels increasingly point at the same type of lender.

Note: The table below reflects historical distinctions. In practice, the lines between traditional hard money and modern professional private lending have largely converged.

What Actually Differentiates Lenders

If the labels have converged, what should a borrower actually be evaluating?

Capital source and depth

Where does the lender's money come from, and how much of it is there? A lender funded by a single family office has different capacity constraints than one backed by a diversified debt fund. When credit markets tighten, lender behavior diverges along capital source lines — some lenders slow down or reprice mid-pipeline, others maintain consistent volume. Asking a lender directly about their capital source is a reasonable due diligence question, and how they answer tells you something.

Underwriting philosophy

Asset-first lenders make decisions based almost entirely on LTV and ARV. Sponsor-aware lenders weight borrower experience, track record, and exit strategy alongside the property. Hybrid lenders run both in parallel. The philosophy affects what deals get done, at what leverage, and at what rate. A first-time investor on a straightforward flip might find an asset-first lender easier to work with. An experienced operator on a complex deal might get better terms from a lender who recognizes the track record.

Operational maturity

Can the lender close when they say they will? Are draw requests processed on schedule? Is there a servicing team that communicates clearly? These questions matter more than the label on the website. Operationally immature lenders, regardless of what they call themselves, create friction that costs borrowers money. A delayed draw on a construction loan can stop work. A failed close can cost an earnest money deposit. The lender's operational infrastructure is part of the product.

Relationship orientation

Some lenders are optimizing for yield on individual transactions. Others are building repeat-borrower businesses where the relationship and the borrower's success matter to the lender's own performance. These orientations lead to different behavior on extensions, workouts, and edge cases. It is worth knowing which type of lender you are working with before something goes sideways.

Matching the Lender Type to the Deal

The choice between lender types is ultimately a deal-level decision. Different situations call for different capital sources.

A time-sensitive acquisition where speed and certainty of close are the primary variables points toward an established professional lender with institutional capital. They have closed thousands of loans. Their process is predictable.

A deal with unusual characteristics — a property type that falls outside standard programs, a borrower situation that needs creative structuring, a market where most lenders won't lend — might require an individual private lender willing to underwrite the specific situation rather than apply a formula.

A fix-and-flip with straightforward rehab scope, a clear ARV, and a borrower with track record is the core product of most professional private lenders. The terms will be standardized, the process will be fast, and the draw management will follow an established protocol.

A DSCR rental loan on a stabilized property is a different product from a bridge loan on a value-add deal, which is a different product from a ground-up construction loan. Lenders specialize. Matching the deal to a lender who does that deal type well matters more than whether they call themselves a hard money lender or a private lender.

Frequently Asked Questions

Is hard money the same as private money?

In practice, increasingly yes. Both terms describe non-bank, asset-based real estate loans. The historical distinction — hard money from professional companies, private money from individuals — has blurred as the industry professionalized. In March 2022, both the NPLA and the AAPL passed formal resolutions urging members to cease using the term "hard money" in favor of "private lending" and "bridge lending." Most professional lenders today use private lending as the umbrella term.

Why do hard money loans have higher interest rates than conventional mortgages?

Several reasons. Private lenders are not deposit-taking institutions, so their cost of capital is higher than a bank's. They accept more risk — shorter terms, value-add properties, borrowers who don't fit conventional criteria. They close faster, which has operational costs. And they operate at smaller scale than major banks, without the same economies. The rate premium is the price of speed, flexibility, and access for deals that can't get conventional financing.

What happened to the term "hard money"?

The industry actively retired it. In March 2022, the NPLA passed a formal resolution discouraging its use, and the AAPL had been pushing in the same direction since its founding. Both associations urged members to remove the term from their websites, marketing materials, and communications. The concern was that "hard money" carried connotations of last-resort, distressed-borrower lending that no longer fit how most professional private lenders operate. "Private lending," "bridge lending," and "transitional lending" are now the preferred terms.

Which is better for a fix-and-flip: hard money or private money?

The term matters less than the lender. For a fix-and-flip, the variables that matter are speed to close, LTV on purchase and rehab, draw management process, and the lender's reliability on construction loans. An experienced professional private lender who does hundreds of fix-and-flip loans per year will outperform an individual private lender with limited experience in that product, regardless of what either calls themselves.

How do I know if a lender is a good fit for my deal?

Ask about their volume in your loan type, their capital source, their draw process, and how they handle extensions. Ask for references from borrowers who have done similar deals. The answers — and the quality of the answers — tell you more than the label on the website.

Baseline is built for professional private lenders: the operators who have moved past informal processes and are building real lending businesses. If you want to see what running a modern lending operation looks like, the demo is at baselinesoftware.com/contact-us