The complete guide to interest calculation methods, per diem, and amortization structures.

Two lenders can offer identical rates on identical loan amounts and produce materially different yields over the life of a portfolio. One configured their day count to 360. The other set it to 365. Neither changed a term sheet yet the gap compounds across every loan they originate.

This guide covers the three most commonly used interest calculation methods in private lending, how per diem works and when it applies, and which amortization structures are standard for each loan product type. Whether you are configuring loan products in an origination system, managing a mixed portfolio of DSCR and construction loans, or reconciling why two identical-rate loans are producing different numbers, understanding the calculations of these interest methods is the difference between the yield you projected and the yield you actually collect.

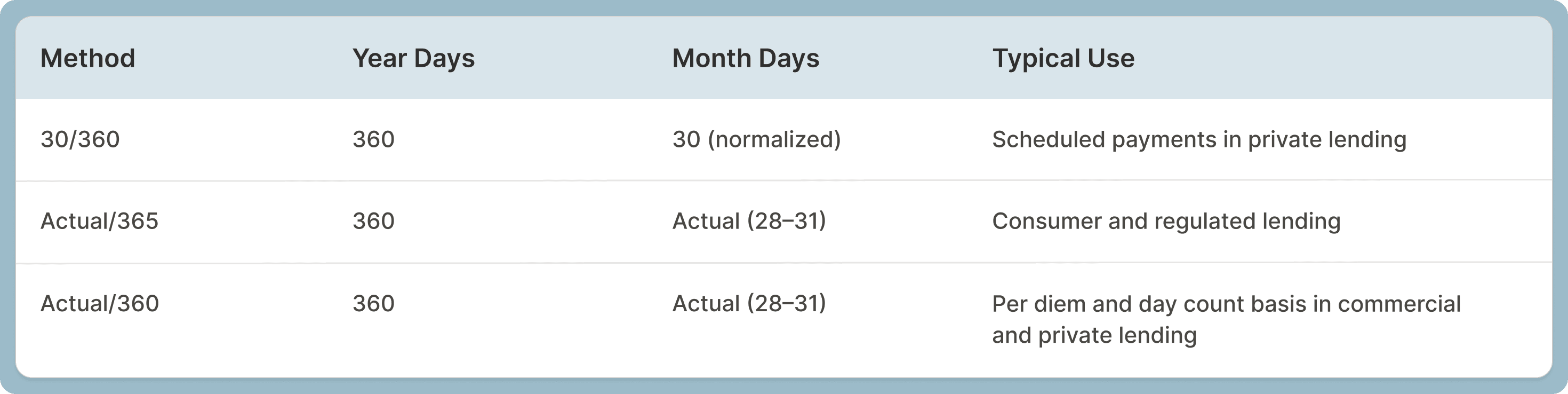

What Are the Three Loan Interest Calculation Methods?

There are three methods most commonly used in private lending and they all use the same stated rate, producing different amounts of interest. The differences come down to two questions: how many days does the year contain for calculation purposes, and how many days does each month contain? The answers determine how much a lender actually earns on every loan they originate.

30/360

The most common method for scheduled payments in private lending. This method normalizes every month to 30 days and every year to 360 days. A $250,000 loan at 12% always produces exactly $2,500 in monthly interest. Payments are predictable, the math is clean, and the effective rate equals the stated rate precisely.

Actual/365

This method uses the real number of days in each month and divides the annual rate by 365. February produces less interest than March. This is the more borrower-friendly structure and is common in consumer lending and regulated mortgage products.

Actual/360

The most common day count basis for per diem calculations in private lending. It uses the real number of days in each month but divides the annual rate by 360 rather than 365. The smaller divisor produces a slightly higher daily rate, which means the lender captures more interest on irregular periods despite the stated rate being identical to an Actual/365 loan.

On a $10,000,000 loan at 8%, the difference between Actual/360 and Actual/365 amounts to approximately $11,111 in additional annual interest in a non-leap year, assuming the balance is outstanding for all 365 days. On a single loan that difference is marginal. Across a full portfolio it becomes a meaningful revenue line.

Why Do Private Lenders Commonly Use the 360-Day Method?

Dividing the annual rate by 360 instead of 365 produces a slightly higher daily rate for per diem calculations. That difference compounds quietly across hundreds of loans and years without changing a single term sheet or negotiating a single basis point with a borrower. It is one of the few yield improvements available to a lender that requires no change to their pricing.

From a borrower's perspective, the difference on a $300,000 loan at 8% amounts to roughly $333 per year, and at 12% roughly $500. Applied consistently across a full portfolio, the 360-day basis produces materially better returns than Actual/365 at the same stated rate.

Multiple courts have enforced clearly drafted Actual/360 clauses when the method is explicitly disclosed in loan documentation. Misleading or ambiguous presentations of the rate as a standard "per annum" figure without adequate clarification have drawn adverse rulings. The cleaner practice is explicit disclosure. One common commercial note formulation reads: the annual interest rate for this note is computed on a 365/360 basis, meaning the ratio of the annual interest rate over a year of 360 days, multiplied by the outstanding principal balance, multiplied by the actual number of days the principal is outstanding.

What Is Per Diem Interest and When Does It Apply in Private Lending?

Per diem is not a fee. It is not a penalty. It is the daily interest rate, applied during the irregular periods that fall outside a standard monthly billing cycle. It most commonly appears in two situations, though the exact circumstances depend on the note and payment schedule.

The two most common situations are:

- The first payment, if the closing date does not land on the first of the month

- The payoff, which almost never occurs on a scheduled payment due date

In private lending, most lenders standardize payment due dates to the first of every month. When a loan closes on the 14th, the borrower owes 17 days of per diem interest at closing to cover the period from the 14th through the 31st. Their first full monthly payment then falls on the first of the following month.

To calculate per diem: multiply the loan amount by the interest rate, divide by the number of days in the year as configured (360 or 365), then multiply by the number of odd days. On a $250,000 loan at 12% using a 360-day year, the daily rate is $83.33. For a 10-day irregular opening period, the per diem charge is $833.33.

The 360 vs. 365 setting directly affects the per diem rate. A lender using Actual/360 will produce a slightly higher daily rate than one using Actual/365 on the same loan. At payoff, the same calculation applies. Borrowers rarely repay on the exact first of the month. A payoff on the 22nd means 22 days of per diem interest for that final period rather than a full monthly payment.

Per diem also applies to newly released draw amounts under non-Dutch construction and fix-and-flip loans. When a draw is disbursed mid-period, interest on that newly released portion is calculated using the per diem rate for the remaining days in the period.

Regular Period vs. Actual Dates: Which Interest Method Should You Use?

Setting the day count basis is the first configuration decision. The second is how to calculate interest for each regular monthly period. This is where most lenders default to whatever their LOS was set to out of the box, and where inconsistencies inside a portfolio quietly start. There are three options, and the choice has real operational consequences.

Regular Period (Most Common)

This method normalizes every month to 30 days for the regular payment calculation. The result is that every interest-only payment is identical regardless of whether a given month has 28, 30, or 31 days. This is the more common approach in private lending. Predictable payments simplify servicing and reduce borrower queries.

Actual Dates

Uses the real number of days in each month to calculate the regular payment. February produces a lower interest payment than March. Less common in private lending but not rare. Some lenders use it when they want the amortization schedule to reflect precise daily accrual rather than a normalized 30-day approximation.

Actual Receive Days

Calculates interest based on when payment is actually received rather than the scheduled due date. Early payment produces slightly less interest for that period. Late payment produces slightly more. The least common configuration in private lending. Most operators avoid it because it creates unpredictability in the amortization schedule and can generate borrower confusion.

Those three decisions, day count basis, interest method, and per diem basis, determine how interest accrues on every loan you originate. But they only address one side of the payment structure. The other side is principal: whether it comes back through regular payments, all at maturity, or on a fixed schedule throughout the loan term. That is where amortization comes in, and it is the third configuration decision that completes the picture for each loan product.

What Are the Three Amortization Types in Private Lending?

Amortization determines how principal is repaid. Worth noting upfront: not all private lending products use amortization at all. Fix-and-flip and construction loans are typically interest-only, meaning the borrower pays interest on the outstanding balance and returns the full principal at maturity. For those products the relevant configuration question is not which amortization type to use, but whether to apply the Dutch or non-Dutch interest method, which is covered in the product-specific section below. For loans that do amortize, primarily DSCR and longer-term bridge, there are three structures. They are not interchangeable, and the right one follows directly from what the loan is for.

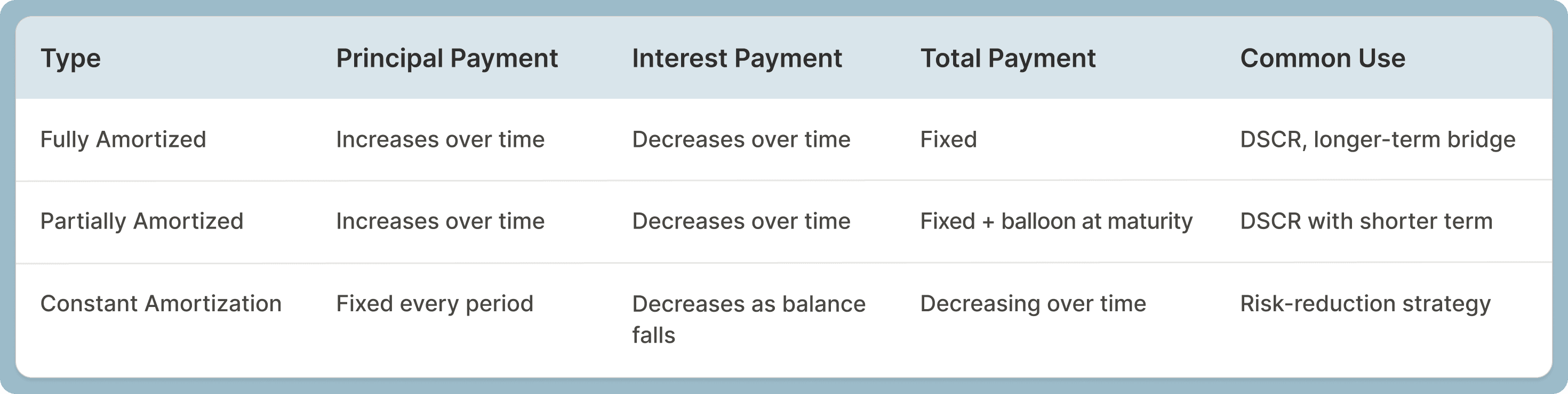

Fully Amortized

A fully amortized loan is the standard mortgage structure. The total payment remains fixed throughout the loan term, but its composition shifts: early payments are heavily weighted toward interest, later payments toward principal. By the final payment, the principal balance reaches exactly zero. The amortization term and the loan term are identical. No balloon payment.

Partially Amortized

Uses the same payment structure as a fully amortized loan, but the loan matures before the amortization period ends. A loan with a 12-month term but 30-year amortization behaves like a 30-year mortgage for 12 months, then requires a balloon payment at maturity to cover the remaining principal balance. The distinction is controlled entirely by whether the amortization term and the loan term are set to the same length.

Constant Amortization

Keeps the principal payment fixed every period. Because the principal balance declines with each payment, the interest portion decreases over time, which means the total payment also decreases. This structure benefits lenders by de-risking the portfolio faster. The borrower's equity position grows more quickly, reducing the lender's exposure as the loan ages. The tradeoff is higher initial payments for borrowers.

Which Structure Is Standard for Each Loan Product?

The question is not which calculation method is theoretically best. It is which method is standard for the product you are offering, because your borrowers, your competitors, and your servicer all operate within those norms. Deviating from them without a reason creates friction. Understanding them lets you configure your products correctly from day one and explain them clearly when borrowers ask.

DSCR Loans

A common configuration is fixed rate, 360-day, fully amortized. Payments are consistent, there is no balloon payment at maturity, and the structure aligns with the DSCR loan's purpose as a long-term hold vehicle for income-generating properties.

The second most common structure introduces an interest-only period, typically the first 5 or 10 years, followed by amortization for the remainder of the term. This configuration exists to manage DSCR qualification. When a property's net operating income does not comfortably cover the fully amortized payment, an interest-only period lowers the initial debt service requirement and allows the loan to qualify at a threshold it would otherwise miss.

Fix-and-Flip and Bridge Loans

These loans are commonly structured as interest-only. No principal is repaid through regular payments. The borrower pays interest monthly and returns the full principal at maturity through a sale or refinance. Bridge loans occasionally carry a principal component but this is the exception. Short term, interest-only, full principal due at maturity is the standard.

For fix-and-flip loans that include a construction or rehab draw component, the Dutch vs. non-Dutch method applies. Under the non-Dutch method, the lender charges interest only on funds that have been released via draws. Under the Dutch method, interest accrues on the full committed loan amount from origination regardless of how much has been disbursed. Non-Dutch is the more common configuration for fix-and-flip with draw components, keeping interest charges aligned with actual capital deployment.

Construction Loans

The same Dutch vs. non-Dutch distinction applies to construction loans.

Under the non-Dutch method, the lender charges interest only on the outstanding drawn balance, not on funds held in reserve pending draw approval. On a $500,000 construction commitment where $200,000 has been released, interest accrues on $200,000 until the next draw is approved and disbursed. Non-Dutch is the standard in private construction lending.

The Dutch method, which charges interest on the full committed balance from origination, does appear in the market. Some lenders use it as an implicit guarantee fee: by committing to the full loan amount, the lender is guaranteeing capital availability, and the Dutch method compensates them for that commitment regardless of draw timing.

How Do Loan Modifications Affect Interest Calculations?

Modifications are where interest calculation errors tend to surface. A rate change or principal adjustment that occurs mid-month splits the period, and if the lender's system does not handle that split correctly, the amortization schedule from that point forward is wrong. Not slightly off. Wrong in a way that compounds through every subsequent payment and creates a dispute at payoff.

For a rate change effective on the 15th: the first 14 days of the period are calculated at the original rate, and the remaining days at the new rate. Each portion is calculated by applying the relevant rate to the actual number of days in that sub-period. The total payment for that month is the sum of both portions.

For a principal balance change: the original balance is used for days before the modification date, and the new balance applies from the modification date forward. The amortization schedule regenerates from the modification date using the updated terms. Lenders who modify loans without recalculating the schedule from that point will produce incorrect projections and potential disputes at payoff.

Why Your Interest Calculation Settings Matter More at Scale

The calculation method, per diem basis, and amortization structure on each product type combine to determine actual portfolio yield: not the yield projected on the term sheet, but the yield that shows up when you reconcile what you expected to collect versus what you actually collected. For most lenders, those numbers are not the same. The gap is usually not fraud or market conditions. It is configuration.

The more significant risk is inconsistency. A lender whose DSCR loans use Actual/360 with 30/360 but whose construction loans were set up with Actual/365 Actual Dates has two different interest engines running in the same portfolio. That inconsistency creates reconciliation complexity, increases the chance of servicing errors, and makes portfolio-level yield analysis unreliable.

Configuring these settings intentionally at the product level, before loans are originated under each product, is the correct approach. The settings should be documented in the lender's credit policy and reflected exactly in the loan origination system so that every loan originated under a given product inherits the correct configuration automatically.

Frequently Asked Questions

What is the most common interest calculation method in private lending?

It depends on what is being calculated. For scheduled monthly payments, 30/360 is the most common method in private lending. It normalizes every month to 30 days, producing identical payments regardless of the calendar month. For per diem calculations on irregular periods such as the first payment and payoff, Actual/360 is the most common day count basis. It uses real calendar days divided by 360, producing a slightly higher daily rate than Actual/365.

Why do private lenders use 360 days instead of 365?

Dividing the annual rate by 360 instead of 365 creates a marginally higher daily interest rate for per diem calculations. On any individual loan the difference is small. Across a full loan portfolio the aggregate effect on annual interest income is significant. Multiple courts have enforced 360-day-based clauses when clearly disclosed in loan documentation.

What is per diem interest and when does it apply?

Per diem interest is the daily interest rate applied to irregular loan periods. It applies when a loan closes on a date other than the first of the month, affecting the first payment, and at payoff, which rarely occurs on a scheduled due date. It also applies to newly released draw amounts under non-Dutch construction and fix-and-flip loans. The per diem rate is derived from the same 360 or 365 day count setting used for those calculations.

What is the difference between fully amortized and partially amortized loans?

In a fully amortized loan, the amortization term and the loan term are identical. The principal balance reaches zero at maturity with no balloon payment. In a partially amortized loan, the amortization term is longer than the loan term. Payments are calculated over a 30-year amortization, for example, but the loan matures at 12 months, requiring a balloon payment to cover the remaining principal balance.

What is the most common amortization structure for each private lending product?

Fix-and-flip and construction loans are typically interest-only. No amortization occurs during the loan term. The borrower pays interest on the outstanding balance and repays the full principal at maturity. For DSCR loans, fully amortized with a 360-day basis is a common structure, though an interest-only period followed by amortization is also widely used when the rental income needs room to meet the DSCR threshold. Bridge loans most commonly mirror fix-and-flip: short term, interest-only, full principal at maturity.

What is the difference between the Dutch and non-Dutch method?

Both methods apply to loans with a draw component, primarily fix-and-flip and construction. The distinction is what balance the lender charges interest on. Under the non-Dutch method, interest accrues only on funds that have actually been released via draws. On a $500,000 commitment where $200,000 has been disbursed, interest accrues on $200,000 only. Under the Dutch method, interest accrues on the full committed balance from origination, regardless of how much has been drawn. Non-Dutch is the standard in private lending. Dutch is used by some

lenders as a guarantee fee structure, compensating them for committing the full capital amount upfront even before draws are made.

How Baseline Handles Loan Product Configuration

Most of the yield leakage described in this article is not the result of bad pricing or weak deal flow. It comes from loan products that were never configured correctly in the first place, and portfolios that have been running on those misconfigured settings ever since. The lender does not know because no single loan looks obviously wrong. The error is only visible when you step back and look at what the portfolio was supposed to earn versus what it actually did.

Baseline builds loan product configuration into the origination system so that every loan inherits the correct interest method, day count basis, amortization type, and construction draw settings from day one. No manual entry per loan. No drift between origination and servicing. If you want to see how that works in practice, request a demo at baselinesoftware.com/contact-us