Bridge loan volume increased 51% year-over-year in January 2025, according to Lightning Docs data drawn from more than half of the nation's top 50 private lenders. The product is not new. The growth is.

What is driving it is not a sudden surge in sophisticated use. It is, in large part, a surge in any use. As more capital has entered private lending and more lenders have expanded their product menus, bridge loans have become a catch-all for deals that don't fit neatly elsewhere. That is where the risk lives.

A bridge loan used correctly is a precision instrument. It solves a specific, time-bounded problem: the gap between where a deal is now and where it needs to be to access permanent financing or achieve a profitable exit. Used loosely, it is a short-term solution to a problem that has not been clearly defined, which is a structure built on an unstated hope rather than an underwritten exit.

This guide defines bridge loans precisely, explains how they are structured and priced, separates them from related products, and gives both lenders and borrowers a framework for when bridge financing is the right answer and when it is not.

What Is a Bridge Loan?

A bridge loan is a short-term, asset-based loan that provides financing during a transitional period. The name is literal: the loan bridges the gap between the current state of a deal and its intended permanent state, whether that is a refinance into long-term debt, a sale, or the completion of a value-add project that makes the asset eligible for conventional financing.

Bridge loans go by several names in the market. Swing loans, gap financing, and transitional loans all describe the same core product. In private lending, bridge and hard money are frequently used interchangeably, though hard money more often signals a specific lender type (asset-based, typically higher rate) than a specific loan structure.

The defining characteristics are consistent across the market:

- Short term: typically 6 to 24 months, with residential bridge loans usually at the shorter end

- Asset-based underwriting: collateral quality drives the credit decision, not primarily borrower income or debt-to-income ratios

- Interest-only payments: the full principal balance is due at maturity, not amortized over the term

- Defined exit: repayment comes from a specific event, sale, refinance, or project completion, not ongoing cash flow

That last point is the one most often underweighted. A bridge loan is not a loan that happens to be short-term. It is a loan explicitly structured around an exit event. The exit strategy is not a secondary consideration. It is the primary underwriting question.

What Bridge Loans Are Actually Used For

The term gets applied broadly. These are the five legitimate use cases, each with a distinct risk profile and exit strategy.

1. Acquiring a New Property Before Selling an Existing One

The most common residential use case. An investor or homeowner identifies a property they want to purchase but has not yet closed on the property they are selling. The bridge loan provides short-term capital to fund the acquisition, secured against the existing property, the new property, or both. The exit is the sale of the existing asset.

For private lenders, this is typically lower-risk bridge lending. The collateral on at least one end is usually a stabilized, marketable asset. The key underwriting question is the liquidity and absorption rate of the market where the existing property is being sold.

2. Transitional Asset Acquisition

An investor acquires a property that does not yet qualify for permanent financing, typically because it is vacant, partially leased, or below market occupancy. The bridge loan finances the acquisition and, in some cases, the stabilization costs. Once the property is stabilized and meets the requirements for a DSCR loan or agency financing, the borrower refinances out.

The exit here is a refinance, not a sale. That means the underwriting question is not what the market will pay for the asset. It is whether the borrower can realistically achieve the occupancy, cash flow, or condition thresholds required by the takeout lender, within the bridge term.

3. Value-Add Repositioning

Similar to transitional acquisition but with a renovation or repositioning component. The investor acquires an underperforming asset, executes a business plan (renovation, re-tenanting, management improvement), and refinances once the asset is performing at a level that supports long-term debt. The overlap with fix-and-flip is real but the intent is typically a hold, not a sale.

4. Construction Completion Bridge

A borrower is partway through a construction or renovation project and their original lender has exited, run out of capital, or declined to fund remaining draws. The completion bridge steps in to fund the remaining work and carry the loan through to a defined exit: a sale or permanent refinance on the completed asset.

This is among the higher-risk bridge use cases for lenders. The collateral value at entry is incomplete by definition, the borrower is often already stressed, and the exit depends on a project being completed successfully by a team that may have already encountered problems. Underwriting discipline and a clear assessment of what remains to be done are essential.

5. Speed-of-Execution Acquisitions

A competitive acquisition where the ability to close in 7 to 10 business days is the deciding factor. The borrower intends to refinance into conventional or agency financing after closing but cannot wait 30 to 60 days for that process to complete. The bridge loan is not a last resort. It is a tactical tool for winning a deal.

The exit is well-defined from day one, the borrower typically has strong credit and liquidity, and the risk is low. This is bridge lending at its most straightforward.

How Bridge Loans Are Structured

Loan-to-Value and Leverage

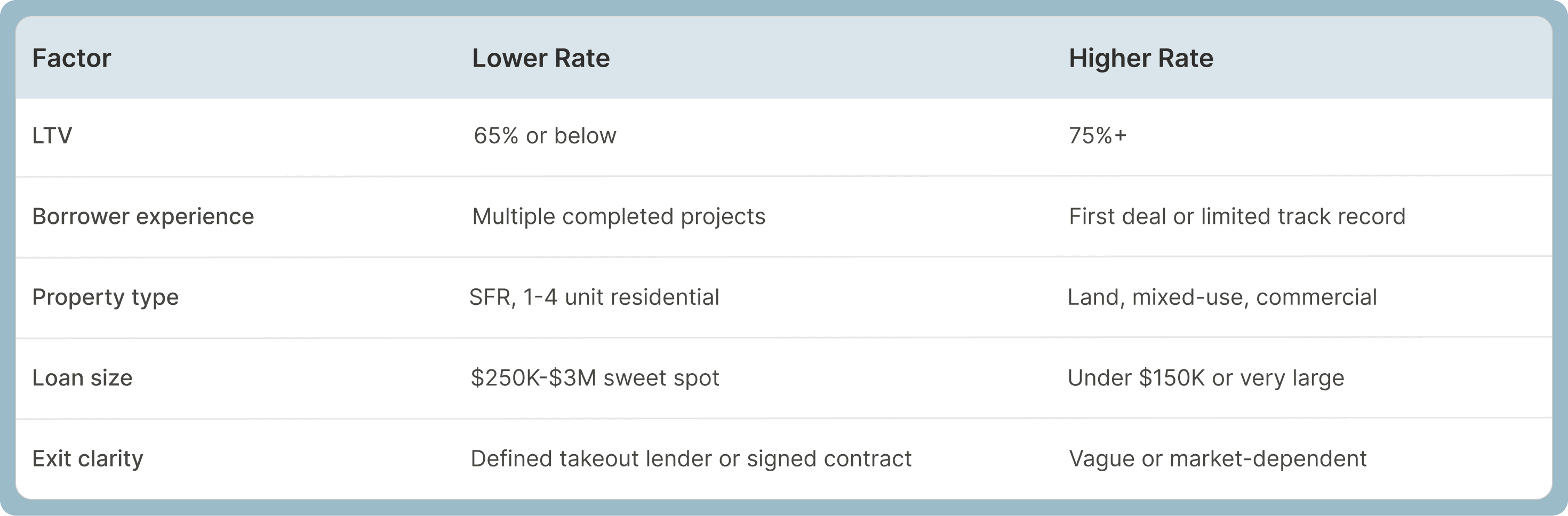

Bridge loans are underwritten primarily on collateral value. For residential investment properties, most institutional lenders have standardized around 65% to 75% LTV. Higher leverage is available from some lenders but typically comes with a meaningful rate premium, reflecting the increased exposure if the exit strategy does not execute as planned.

For commercial bridge loans, LTV ranges vary more widely by asset type. Multifamily and mixed-use assets with predictable income may support higher leverage. Land and transitional commercial properties typically sit at the lower end.

When a renovation or repositioning component is involved, lenders use LTC (loan-to-cost) and LTARV (loan-to-after-repair-value) alongside as-is LTV to determine the appropriate loan amount. The same principle applies as in fix-and-flip underwriting: the most conservative ratio controls.

Interest-Only Structure

Bridge loans do not amortize. The borrower pays interest monthly on the outstanding balance and repays the full principal at maturity. This keeps monthly carrying costs lower during the project phase, which matters for deals where the asset is not yet generating income sufficient to service amortizing debt.

The implication for lenders is that the principal balance does not decrease over the loan term. The risk at month 18 of a 24-month loan is structurally similar to the risk at month one. That makes the exit strategy evaluation at underwriting more consequential, not less.

Points and Fees

Origination points typically run 1 to 3 on bridge loans, depending on lender, loan size, borrower profile, and market. Repeat borrowers with established lender relationships often negotiate reduced points over time. On larger loans, even a half-point reduction represents meaningful dollars.

Total cost of capital is the number that matters, not headline rate alone. A loan at 10.5% with 2 points on a 12-month term costs more than a loan at 11% with 1 point. Borrowers should calculate the full annualized cost of capital across the expected hold period before comparing term sheets.

Extensions

Most bridge lenders offer extension options for borrowers who need additional time beyond the original term. Extensions are not automatic. They require the lender's approval, typically involve an extension fee (0.5 to 1 point is common), and may trigger a rate adjustment.

For lenders, an extension request is a credit event, not an administrative process. It signals that the original exit timeline did not hold. The question is whether the revised timeline is credible, whether the underlying asset has maintained or improved in value, and whether extending is a better outcome than initiating a default process.

Disciplined lenders treat extension decisions with the same rigor as original underwriting. Lenders who approve extensions reflexively, without re-evaluating the exit thesis, are accumulating risk that does not show up in their portfolio until it does.

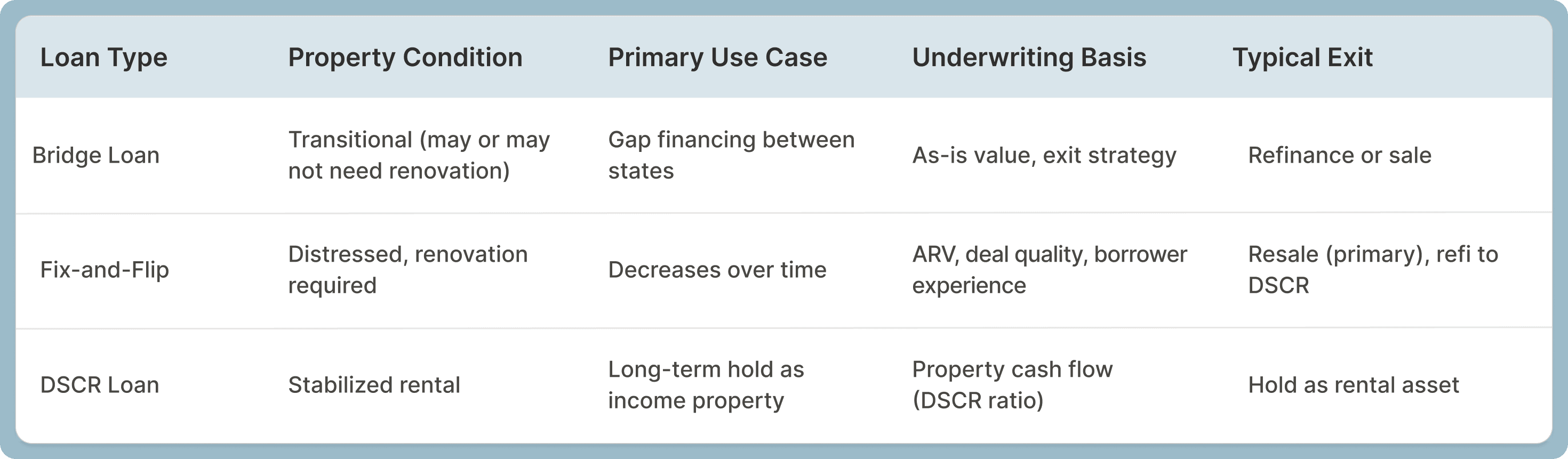

Bridge Loans vs. Fix-and-Flip Loans vs. DSCR Loans

These three products are frequently confused. The distinctions are operationally meaningful.One clarification worth making: fix-and-flip loans are technically a subset of bridge financing. Both are short-term, asset-based, and structured around a defined exit. The distinction is that fix-and-flip lending centers on a renovation thesis and an ARV-based underwriting model, while bridge lending is the broader category that encompasses any transitional situation, including those with no renovation component at all.

The bridge-to-DSCR strategy has become increasingly common in today's compressed-margin environment. An investor who acquires a property intending to flip it may, if resale margins narrow during the hold period, choose to stabilize it as a rental instead and refinance into a DSCR loan. Lenders who originate both products are positioned to serve both legs of that transaction. The lender who only does bridge sends the borrower elsewhere for the second origination.

Bridge Loan Rates and Costs in 2026

Rate clarity is harder to find in bridge lending than in most loan categories. Lenders quote ranges because bridge loans are genuinely deal-specific in a way that fixed-rate products are not. The range is real, but it is not as wide as it sometimes appears.

For well-structured residential investment deals with experienced borrowers, rates in the current market run 9% to 11%. The national average, drawn from Lightning Docs transaction data, was 10.43% in September 2025, down from 11.1% a year earlier. Most deals price in the 9% to 12.99% range, with the distribution clustering around 10% to 11% for mainstream residential bridge.

Rates above 12% reflect one or more of the following: first-time borrowers, higher leverage, land or unusual collateral, markets with weaker absorption, or lenders with higher cost of capital. Rates below 9% are available from some institutional programs on clean, low-leverage deals with strong borrower profiles.

Points at origination typically run 1 to 3. Total cost of capital on a 12-month bridge at 10.5% with 2 points is approximately 12.5% annualized, which is the number that should be used in deal proformas, not the headline rate.

Rate stability heading into the remainder of 2026 is expected. Pricing is no longer driven by rapid Fed movements, as it was in 2022 and 2023. Deal fundamentals, leverage, and borrower profile now dominate the pricing decision, which makes rate outcomes more predictable at underwriting.

What Private Lenders Evaluate When Underwriting a Bridge Loan

Bridge loan underwriting has three pillars: the collateral, the exit, and the borrower. In that order of priority.

The Collateral

As-is value is the starting point. For residential assets, lenders rely on BPOs, AVMs, or full appraisals depending on loan size and complexity. For commercial assets, a full appraisal is standard. The collateral evaluation also includes property condition, marketability (how quickly could this asset be sold or refinanced in a distressed scenario?), and local market dynamics.

Properties in markets with high inventory growth, slow absorption, or declining values carry more risk in a bridge portfolio because a failed exit strategy leaves the lender holding an asset that is harder to recover against. Geographic concentration in these markets deserves ongoing portfolio scrutiny.

The Exit Strategy

This is the most important variable in bridge underwriting, and the one most frequently evaluated superficially.

A vague exit strategy is not an exit strategy. "We plan to refinance" is not sufficient. The underwriting question is: refinance to what product, with which lender, subject to what conditions, and is the borrower currently on a path to meeting those conditions within the loan term?

A sale exit requires evaluation of the local market's absorption rate, the price point the borrower expects to achieve, and whether current comparable sales support that number. A refinance exit requires understanding the underwriting criteria of the likely takeout lender, including their occupancy, DSCR, or condition requirements, and assessing whether those thresholds are achievable within the bridge term.

Lenders who approve bridge loans on vague exit strategies are not underwriting. They are hoping.

The Borrower

Borrower profile matters in bridge lending, though it plays a secondary role to collateral and exit. The key variables are experience (has this borrower successfully executed similar projects?), liquidity (do they have adequate reserves to carry the project through unexpected delays?), and credit (minimum FICO thresholds typically run 650 to 680, with better pricing available above 720).

For construction completion bridges and value-add repositioning deals, the borrower's track record with similar projects is weighted more heavily. A borrower who has successfully repositioned three multifamily assets is a meaningfully different credit profile than one who has not, even if the collateral looks identical on paper.

Bridge Loan Risks: What Lenders and Borrowers Need to Understand

For Borrowers

The rate premium over permanent financing is real. A bridge loan at 10.5% costs more than a DSCR loan at 7.5%, and that difference accumulates quickly on a 12 to 18 month hold. Bridge financing is justified when speed, flexibility, or the transitional nature of the asset leaves no permanent financing option available. It is not justified simply because it is easier to get than conventional debt.

Maturity default risk is the most serious risk borrowers face. A bridge loan that cannot be repaid at maturity because the exit strategy did not execute as planned is a default. Extensions require lender approval and come with costs. Lenders are not required to extend, and some will not. Borrowers who treat the bridge term as flexible are misunderstanding the product.

For Lenders

The principal balance on a bridge loan does not decrease over the term. If the market softens, the asset deteriorates, or the borrower's business plan does not execute, the lender's collateral position has not been gradually strengthened by amortization. It is the same position it was at origination, possibly in a worse market.

Extension creep is a portfolio risk that develops slowly and becomes visible all at once. A lender with a large proportion of extended loans is carrying concentration risk in deals where the original thesis did not hold. Regular portfolio review of extension rates, by vintage, product type, and geography, is a risk management practice, not an administrative formality.

The distinction between a bridge loan that is the right product for the situation and a bridge loan that is a fix for a deal that did not underwrite correctly often becomes clear at extension time. Building that discipline into the original credit decision is cheaper than building it into the workout process.

Frequently Asked Questions

How is a bridge loan different from a hard money loan?

The terms are often used interchangeably, but they describe slightly different things. Hard money refers to asset-based lending from private sources, typically at higher rates and with faster execution than conventional lenders. Bridge loan refers to the structure and purpose: short-term financing for a transitional situation. A hard money lender often originates bridge loans. Not every bridge loan comes from a hard money lender. The overlap is significant but not complete.

What credit score do you need for a bridge loan?

Most private bridge lenders require a minimum FICO in the 650 to 680 range, with better pricing available above 720. Because bridge lending is primarily asset-based, credit score plays a supporting role rather than a controlling one. A borrower with a 660 FICO and a well-structured deal with a clear exit will generally get funded. A borrower with a 740 FICO and a poorly structured exit will not.

Can you get a bridge loan on a commercial property?

Yes. Commercial bridge loans are a meaningful segment of the private lending market, particularly for multifamily value-add acquisitions, office conversions, and retail repositioning. Terms, leverage, and rates vary by asset type. Multifamily assets typically support better terms than retail, office, or mixed-use, reflecting differences in liquidity and execution risk. Underwriting for commercial bridge is generally more complex and documentation-intensive than residential.

How fast can a bridge loan close?

Private bridge lenders typically close in 7 to 14 business days when documentation is complete. Some lenders close in as few as 5 business days on straightforward residential deals with experienced, organized borrowers. The main variables are valuation timing, title, and documentation completeness. For commercial bridge loans, timelines typically run 10 to 21 days due to additional due diligence requirements.

What happens if you cannot repay a bridge loan at maturity?

A bridge loan that cannot be repaid at maturity is in default. The lender has several options: approve a formal extension (typically requiring a fee and possibly a rate adjustment), work with the borrower toward a modified payoff arrangement, or begin enforcement proceedings, including foreclosure. Lenders are not obligated to extend. Borrowers who anticipate difficulty repaying at maturity should communicate with their lender as early as possible. Lenders generally prefer a structured resolution over a protracted default process, but they are under no obligation to offer one.

How Baseline Supports Bridge Lenders

Bridge lending is operationally straightforward compared to fix-and-flip or construction, but the loan lifecycle still requires active management: tracking maturity dates, managing extension decisions, monitoring collateral values, and maintaining clear borrower communication across multiple active loans simultaneously.

Baseline is built for private lenders who originate bridge loans at scale. The platform handles the full loan lifecycle from origination through payoff, with portfolio-level reporting that gives lenders real-time visibility into maturity exposure, extension history, and geographic concentration.

See how Baseline works for bridge lenders at https://www.baselinesoftware.com/contact-us