Platform evaluations tend to go well right up until implementation. The demo is clean, the feature list is long, and the pricing looks reasonable. What rarely surfaces in a 45-minute walkthrough is whether the platform correctly handles the mechanics that actually define private lending — interest calculation configuration by product, non-Dutch draw accrual, split-period loan modification recalculation, investor capital management. These are the capabilities that determine whether a platform works in practice.

The ten features below are the ones that separate a platform built for private lending from one that was adapted for it. Each item names the specific capability, explains why it matters for this asset class specifically, and describes what it looks like when a platform handles it incorrectly. The quick-reference checklist at the end is built to use in any platform evaluation — bring it into a demo and ask for live demonstrations of each item, not descriptions.

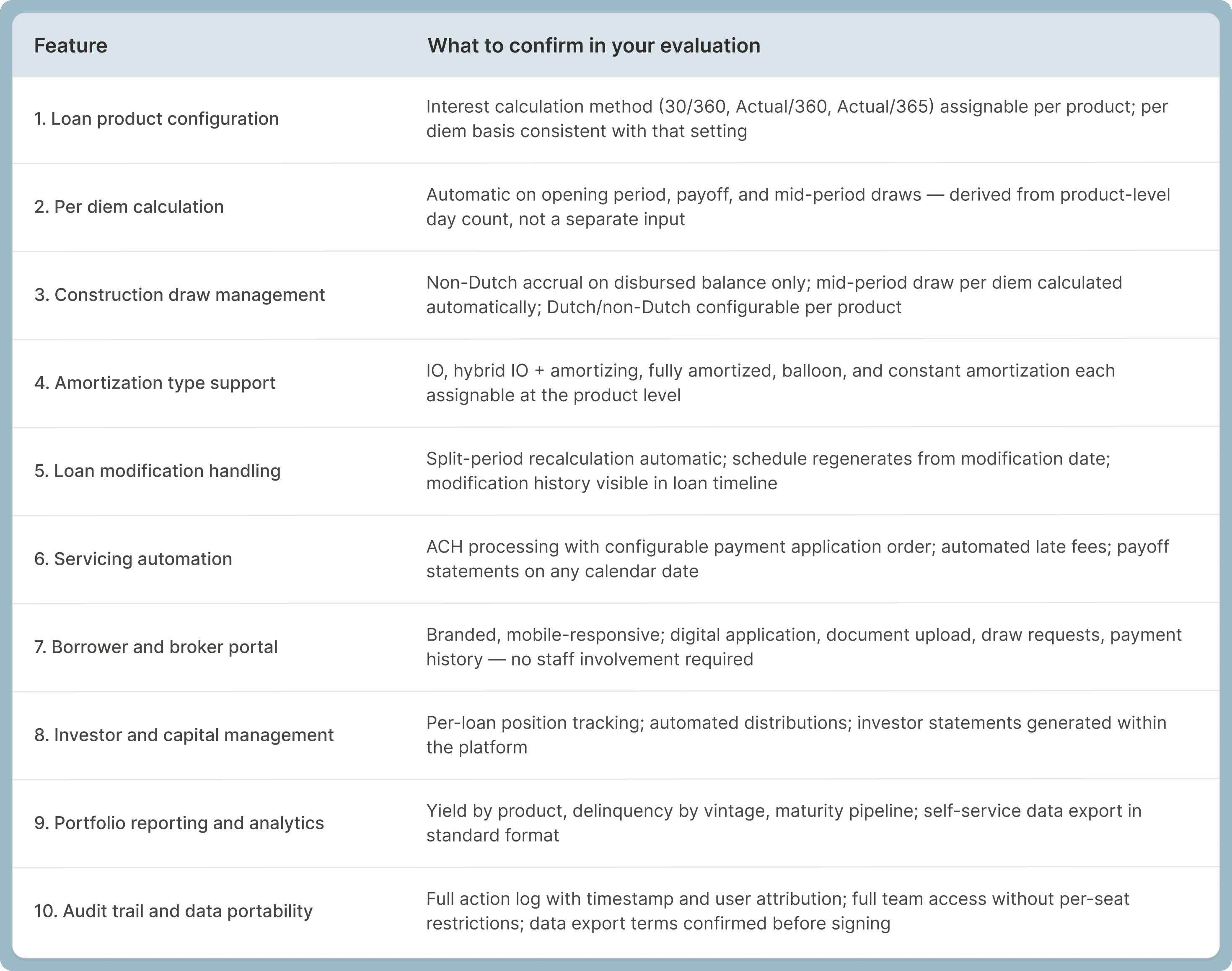

1. Loan Product Configuration with Interest Calculation Method Assigned at the Product Level

WHY IT MATTERS

Private lending usually uses three interest calculation methods: 30/360, Actual/365, and Actual/360. Each is a legitimate choice for specific products and purposes. The question is not which method a lender uses — it is whether the platform enforces that choice consistently across every loan originated under a given product. A misconfigured or inconsistently applied product setting on a $10,000,000 portfolio at 8% produces a calculation discrepancy of approximately $11,111 per year between the two Actual methods. That gap does not appear on any individual loan statement. It surfaces only when projected yield is compared against what the portfolio actually collected.

WHAT TO LOOK FOR

The ability to configure the interest calculation method, per diem basis, amortization type, and fee structure at the product level — so every loan originated under a given product inherits the correct settings automatically, without manual override per loan. Fee types (origination, extension, exit, draw, inspection) should be configurable and automatically posted to the loan ledger rather than tracked separately.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

The interest method is set globally rather than per product, or defaults to a single setting that cannot be changed without technical support. Lenders running multiple product types on a misconfigured platform often do not discover the error until a portfolio-level reconciliation reveals that projected yield and actual yield do not match — at which point the error has been compounding across every loan originated under that product.

2. Automated Per Diem Calculation for Irregular Periods

WHY IT MATTERS

Per diem interest applies in three situations: the opening period when a loan closes on a date other than the first of the month, the payoff calculation when a borrower repays before their next scheduled due date, and on newly released draw amounts when a disbursement occurs mid-period. These irregular periods occur on nearly every loan in a private lending portfolio. In a platform that does not handle them automatically, per diem is calculated manually — which means it is calculated inconsistently, estimated, or missed entirely.

WHAT TO LOOK FOR

Automatic per diem calculation on the opening period, the payoff statement, and mid-period draw disbursements. The per diem rate should derive from the same day count setting configured at the product level — 360 or 365 — not from a separate input or a platform-wide default that may not match the product's configuration. These should be the same setting, applied consistently throughout the loan lifecycle.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

Per diem appears as a field the lender must calculate and enter manually at closing and payoff. The rate used for per diem does not match the product's configured day count, creating a systematic discrepancy between regular period interest and irregular period interest across the portfolio. Because per diem calculations are irregular by nature, they are the least likely part of a lending operation to be audited — which is exactly where errors accumulate without surfacing.

3. Construction Draw Management with Non-Dutch Interest Accrual

WHY IT MATTERS

Under the non-Dutch method — standard in private construction and fix-and-flip lending — interest accrues only on funds that have been disbursed, not on the full committed loan amount. On a $500,000 construction commitment where $200,000 has been released, interest accrues on $200,000. When a draw of $75,000 is released mid-period, interest on that newly disbursed amount accrues at the per diem rate for the remaining days in the period. A platform that cannot track draw disbursements and automatically calculate interest on the released balance will produce incorrect interest charges on every draw-based loan in the portfolio.

WHAT TO LOOK FOR

A draw disbursement workflow with approval routing, budget tracking, and automatic interest accrual on the disbursed balance only. When a draw is released mid-period, the platform should automatically calculate the per diem charge for the remaining days and reflect it in the current period's total — without manual input. Dutch versus non-Dutch should be configurable at the product level for lenders who use both structures.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

Interest accrues on the full committed balance from origination regardless of how much has been drawn, or draw tracking requires manual balance updates before interest calculates correctly. Either failure produces inflated interest charges. The discrepancy typically goes unnoticed until payoff, when the gap between what the system shows and what the borrower expects is largest — and hardest to resolve quickly.

4. Full Amortization Type Support

WHY IT MATTERS

Private lending uses at least four distinct payment structures. DSCR loans are typically fully amortized or partially amortized with a balloon payment at term. Fix-and-flip and bridge loans are typically interest-only, with full principal due at maturity. Some lenders use constant amortization — a fixed principal payment each period, with decreasing total payments as the balance falls — for risk management purposes. A platform that supports only one or two of these structures cannot serve a mixed-product portfolio without workarounds, and workarounds in amortization calculations compound into servicing errors over the life of the loan.

WHAT TO LOOK FOR

Interest-only configuration with full principal due at maturity; fully amortized configuration where the amortization term and loan term are identical; partially amortized configuration where the loan matures before the amortization period ends, requiring a balloon payment; and constant amortization where the principal component is fixed each period. Each type should be assignable at the product level, not configured loan by loan.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

The platform supports one primary structure and approximates others through manual field overrides. Balloon payments are entered as custom amounts rather than generated from the amortization configuration. Lenders discover the limitation when a product type they want to offer requires capabilities the platform cannot support natively — usually at the point of origination, when it is too late to reconfigure without disrupting the deal.

5. Loan Modification Handling with Split-Period Recalculation

WHY IT MATTERS

A rate change or principal adjustment effective mid-period splits the billing cycle. Interest for days before the modification date accrues at the original terms; interest for days after accrues at the new terms. If the platform does not handle this split automatically — and does not regenerate the amortization schedule from the modification date forward — it produces an incorrect schedule from that point. Every subsequent payment is calculated against a wrong baseline. The error is small in any individual period but compounds through the remaining loan term, and becomes visible as a balance discrepancy at payoff. Resolving it at that point requires manual reconstruction of the payment history — an operationally expensive outcome for what was originally a routine modification.

WHAT TO LOOK FOR

Automatic split-period interest calculation when a modification is effective on any date other than the first of the month. Amortization schedule regeneration from the modification date using the updated terms. A full audit trail of the modification — who made it, when, and what changed — accessible within the platform without a support request.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

Modifications are recorded but the schedule is not regenerated. The platform displays a correct-looking amortization table that is wrong from the modification date forward. The error only becomes visible at payoff, when the scheduled remaining balance does not match the actual remaining balance — at which point it must be corrected manually under time pressure, often in a borrower-facing context.

6. Servicing Automation — Payments, Late Fees, and Payoff Statements

WHY IT MATTERS

Servicing is where the configuration decisions from features one through five either hold or expose themselves. A platform that calculates interest correctly at origination but cannot process payments automatically, apply them in the correct order, or generate an accurate payoff statement on demand has solved the easier half of the problem. Past a certain portfolio size — typically somewhere between 50 and 100 loans depending on product complexity — manual servicing stops being a workflow choice and becomes a capacity ceiling.

WHAT TO LOOK FOR

Automated ACH payment processing with configurable payment application order — most private lenders apply payments to interest first, then principal, then fees, but this should be configurable rather than hardcoded. Automated late fee calculation and posting tied to the grace period set at the product level. Payoff statement generation on any calendar date, including per diem through the payoff date, without manual calculation. Automated notices for payment due, past due, and payoff confirmation.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

Payoff statements require manual calculation or can only be generated as of a scheduled due date. Payment application order is fixed by the platform rather than configurable. Late fees are tracked outside the system because the platform cannot post them automatically. Each of these gaps adds staff time per loan per month, and the cumulative cost scales directly with portfolio size.

7. Borrower and Broker Portal

WHY IT MATTERS

Private lending competes on speed. A lender whose borrowers submit documents by email, request draws by phone, and wait for manually generated payoff statements is giving back a meaningful portion of that speed advantage on every loan — and signalling to borrowers that the operation behind the rate is not as professional as the rate itself. Once a portfolio reaches the scale where software becomes necessary, a borrower portal is less an amenity than a staffing decision: without it, every borrower question and draw request requires human handling.

WHAT TO LOOK FOR

A branded borrower portal — not a generic white-label interface — where borrowers can complete applications digitally, upload required documents, track loan status, submit draw requests with supporting documentation, view payment history, and access upcoming payment obligations. Mobile-responsive design is a requirement, not an option. For lenders who source deals through brokers, a broker portal where partners can submit deals, track pipeline status, and communicate without involving internal staff adds meaningful operational leverage in competitive origination markets.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

The borrower portal exists as a marketed feature but requires the lender's staff to manage document collection and status communication on the borrower's behalf. Draw requests still come in by phone or email. The portal is desktop-only or requires the borrower to download a separate application. Brokers have no pipeline visibility without calling the lender directly.

8. Investor and Capital Management

WHY IT MATTERS

Most private lenders deploy capital from investors. Managing investor positions, calculating returns, and distributing proceeds in a spreadsheet works at a small number of relationships and becomes operationally unreliable as that number grows. The failure mode is predictable: investor reporting is the last task to get done, the first to contain errors, and the most damaging to get wrong. In 2026, LP expectations for self-service access and timely reporting have risen considerably — investors working with multiple managers can immediately distinguish operations that send portal links from those that send spreadsheet attachments.

WHAT TO LOOK FOR

Per-loan investor position tracking; automated return calculation based on configured investor terms; a distribution workflow that processes payouts without requiring manual calculation; investor statements generated within the platform rather than assembled externally. For lenders operating fund structures — mortgage investment corporations, debt funds, syndicated deals — the platform should support capital call tracking, preferred return calculations, and waterfall distributions. An investor portal with self-service access to positions, returns, and distribution history reduces inbound communication volume and signals operational maturity to capital partners.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

Investor reporting lives in a spreadsheet outside the platform. Distributions are calculated manually at the end of each period. Investors receive statements by email that were assembled in Excel. The lender cannot answer a question about an investor's current position without opening a separate file — which creates the exact kind of friction that erodes investor confidence over time.

9. Portfolio Reporting and Analytics

WHY IT MATTERS

A lender who cannot see yield by product type, delinquency by loan vintage, or the maturity pipeline for the next 90 days is making portfolio decisions without the information those decisions require. Reporting is also where the configuration accuracy from features one through five becomes verifiable: if interest calculation has been misconfigured at the product level, yield by product will expose it. If servicing has been inconsistent, delinquency by vintage will surface the pattern. Reporting is not just an output — it is the mechanism through which configuration errors become visible before they become disputes.

WHAT TO LOOK FOR

Yield by loan product; delinquency and past-due tracking with aging buckets; maturity schedule showing upcoming balloon payments and loan expirations; draw budget utilization for the construction and fix-and-flip portfolio; investor return reporting by investor and by loan; portfolio-level cash flow projection. Critically: the ability to export all of this data in a standard format — CSV or structured data — without a support request or additional fee. Reporting locked to the platform's own interface cannot be shared with capital partners, auditors, or board members who need it in a different format.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

Reports are available but limited to the platform's own interface. Data cannot be exported without opening a ticket or paying a fee. The available reports do not map to the metrics the lender actually tracks. Portfolio-level yield analysis requires pulling data from the platform and processing it in a separate spreadsheet — which reintroduces the same problem the software was supposed to solve.

10. Audit Trail and Data Portability

WHY IT MATTERS

Every payment posted, every modification made, every manual override applied should be logged with a timestamp and user attribution. In a borrower dispute, a regulatory inquiry, or an institutional due diligence review, a complete audit trail is the difference between a defensible record and a manual reconstruction exercise. Data portability matters for a separate and equally practical reason: your ability to retrieve your complete loan history in a usable format — if you switch platforms, engage a new servicer, or respond to a capital partner's data request — should not require a negotiation with the vendor. It should be self-service.

WHAT TO LOOK FOR

A complete audit log on all loan-level actions, accessible to the lender within the platform without a support ticket. Data export in CSV or another standard format, available on demand and without additional fees. No lock-in mechanisms that restrict access to your own data. During any platform evaluation, request a full data export of a sample loan and verify the format and completeness before signing anything.

WHAT IT LOOKS LIKE WHEN A PLATFORM GETS IT WRONG

The audit trail exists but is accessible only to the vendor's support team. Data export requires a formal request, a processing window of several days, or an additional fee. The exported data is formatted for the platform's own import process rather than for general use. Lenders who discover these limitations after signing face a choice between staying on a platform where they cannot freely access their own data or absorbing significant switching costs to leave.

What This List Reveals

The ten features above share a common logic: each is a capability where a platform either handles the private lending mechanic correctly from configuration, or creates a workaround that introduces error, absorbs staff time, and compounds across the portfolio. None of them are advanced features. They are the baseline operational requirements of a platform built specifically for this market.

A platform that handles all ten correctly does not guarantee performance — execution, team training, and credit policy still matter. But a platform that handles even two or three of them incorrectly will produce yield leakage, servicing errors, or investor reporting failures that no amount of manual effort fully corrects. The checklist below is built to use in a demo room. Bring it, ask the questions, and require live demonstrations rather than descriptions.

What features should I look for in private lending software?

The features that matter most in private lending are the ones that map to the specific mechanics of the asset class: product-level interest calculation configuration, automated per diem for irregular periods, non-Dutch draw accrual for construction and fix-and-flip loans, full amortization type support, and automatic split-period recalculation for loan modifications. These are distinct from the general LOS capabilities that appear on most vendor feature lists — and they are the ones most likely to separate platforms that work for private lending from those that approximate it.

What is loan product configuration in private lending software?

Loan product configuration is the process of setting the interest calculation method, day count basis, amortization type, per diem basis, and fee structure at the product level — so that every loan originated under a given product inherits those settings automatically. In a well-configured platform, a DSCR product and a fix-and-flip product each carry their own settings, and no manual override is required per loan. In a platform that does not support product-level configuration, these settings must be applied per loan or set globally — both of which introduce inconsistency and the risk of calculation errors across the portfolio.

What is the most important feature to look for in private lending software?

Loan product configuration — specifically, whether the platform can assign the interest calculation method, per diem basis, and amortization type at the product level. This single capability determines whether every loan in the portfolio calculates correctly from origination. A platform that handles configuration incorrectly or inconsistently introduces yield errors that compound silently and are difficult to diagnose after the fact.

Does private lending software need to handle construction draws differently than a standard LOS?

Yes. Standard loan origination systems are not designed for the non-Dutch draw accrual method standard in private construction and fix-and-flip lending. A general LOS that accrues interest on the full committed balance from origination — rather than on disbursed funds only — will produce inflated interest charges on every draw-based loan in the portfolio. This is one of the most common points of operational failure for private lenders who select a conventional platform rather than one built for their product types.

What is the difference between a loan origination system and loan servicing software?

A loan origination system manages the loan creation process — application, underwriting, document generation, and closing. Loan servicing software manages the loan after closing — payment processing, interest accrual, draw management, investor reporting, and payoff. Some platforms cover both in a single system; others specialize in one and integrate with a partner for the other. For most private lenders, a single platform handling the full lifecycle is operationally simpler and reduces the risk of misconfiguration at the handoff between systems.

How Baseline Addresses These Features

The ten features in this list reflect the operational requirements of a private lending business running at scale — not a wishlist, but the capabilities a platform needs to handle this market correctly. Baseline is built around these requirements: loan product configuration at the product level, automated per diem across all irregular periods, non-Dutch draw accrual, full amortization type support, automatic split-period modification handling, servicing automation, borrower and broker portals, investor management, portfolio reporting, and complete audit trail with self-service data export.

If you want to test any of these against your specific loan products and workflows, request a demo at baselinesoftware.com/contact-us