What is private lending?

Ask an investor who closed a deal in nine days and you'll get one answer. Ask someone who got turned down by three banks on the same property and you'll get another. Alexandria Breshears and Beth Johnson, who wrote the book on it — literally, Lend to Live — describe it as what used to be a trade secret for corporate lenders, now available to anyone willing to learn how it works.

The US private lending market originated approximately $121 billion in business-purpose real estate loans in 2025, up from $97 billion in 2024, according to SFR Analytics — roughly 14 percent year-over-year growth. Zooming out, the global private credit market, which encompasses real estate debt alongside corporate direct lending and infrastructure, reached $3.5 trillion in assets under management in 2025 according to the Alternative Credit Council, with Morgan Stanley projecting $5 trillion by 2029. Private lenders financed 18 percent of all SFR corporate property purchases in 2025, up from 15 percent in 2024, as banks have continued to pull back from real estate investment lending under tighter regulatory pressure since 2008.

For real estate investors, that growth means more options, more capital, and more lenders competing for business. Understanding how private lending works is no longer a specialty skill. It is table stakes.

How Private Lending Works

The mechanics are straightforward. A borrower needs capital to acquire, renovate, or bridge a property. They approach a private lender, who evaluates the deal primarily on one question: does the asset support the loan?

Private lenders use several metrics to evaluate how much to lend. The most common are loan-to-value (LTV), which divides the proposed loan amount by the property's current value, and loan-to-ARV (LTARV), which uses the projected after-repair value for fix-and-flip deals. For ground-up construction and heavy rehab projects, loan-to-cost (LTC) — the loan as a percentage of total project cost — is often the primary lens. Each metric sets a ceiling on how much a lender will advance, and multiple metrics may apply to the same deal. The specific thresholds vary by lender, loan type, and market conditions.

Beyond the numbers, lenders typically look at the borrower's exit strategy, their experience with similar projects, and their liquidity. A strong deal with a clear exit can overcome a thin credit file. A weak asset does not get rescued by a strong borrower.

The transaction closes with a promissory note, a mortgage or deed of trust securing the lender's position, and a loan agreement defining the rate, term, and repayment structure. For interest-only loans — the most common structure in bridge and fix-and-flip lending — the borrower pays interest monthly and repays the full principal at maturity, upon sale, or upon refinance. For amortizing loans such as DSCR rental loans, a portion of principal is returned with each monthly payment.

Private lenders come in numerous forms: individual high-net-worth investors deploying personal capital, private lending companies funded through institutional channels or their own balance sheets, and debt funds pooling capital from multiple investors, to name the most common. Each operates somewhat differently, but the core underwriting logic is the same.

Private Lending vs. Traditional Financing: Where the Difference Actually Shows Up

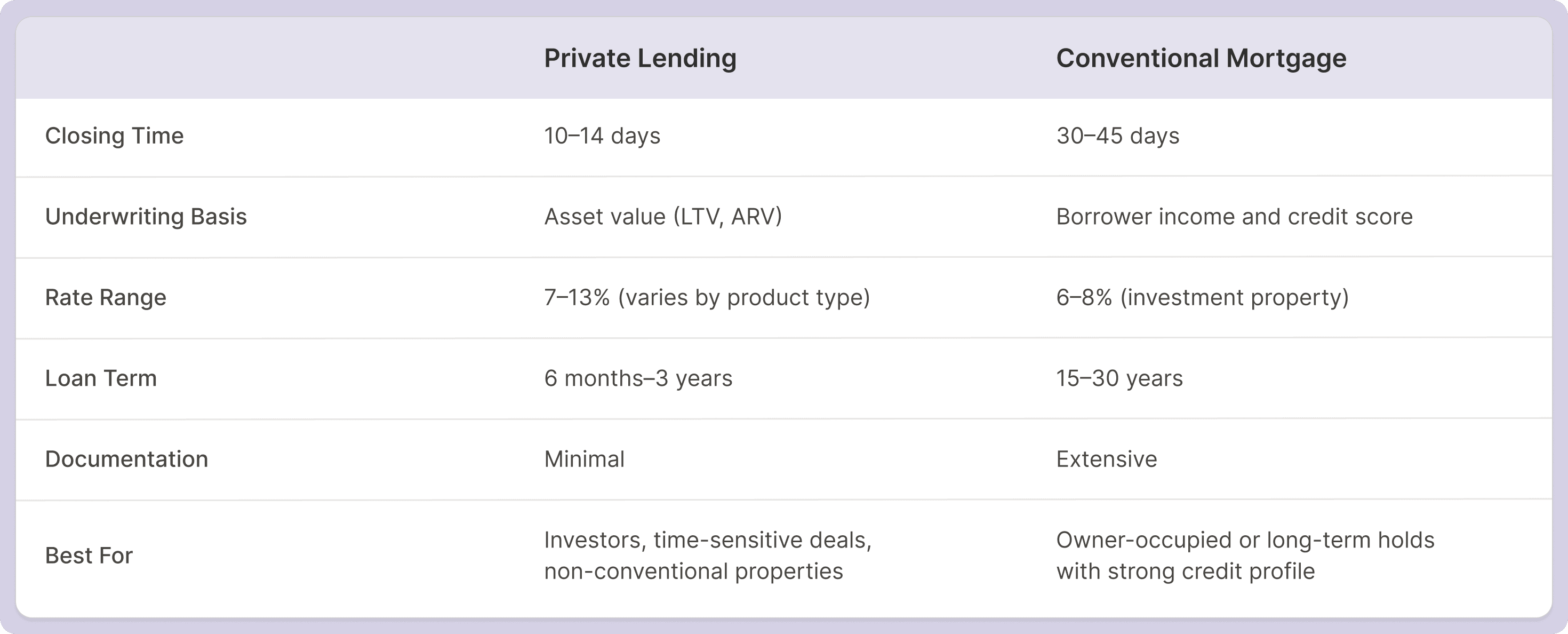

The speed gap is the most obvious difference, and it is significant. Conventional mortgages for investment properties typically take 30 to 45 days to close, assuming a clean file and no complications. Private loans close in 10 to 14 days in most cases, and faster-moving lenders can close in 5 to 7 days on straightforward deals.

For real estate investors, that gap is often the margin between winning and losing a deal.

The underwriting gap matters just as much. Conventional lenders verify income, analyze debt-to-income ratios, run credit pulls, and require properties to meet specific condition standards. A fix-and-flip property in disrepair cannot get conventional financing. A self-employed investor with variable income will struggle even if their track record is strong. A borrower who needs to close in 10 days will not get there through a bank.

Private lending sidesteps all of that. The loan is backed by the asset, not the borrower profile.

The tradeoff is cost. Rate ranges vary by product: bridge and fix-and-flip loans typically run 9 to 13 percent in the current environment, while DSCR rental loans for stabilized properties generally fall in the 7 to 9 percent range. Origination fees are typically 1.5 to 3 points. Terms are short on bridge products, generally 6 months to 3 years, which means the borrower needs a clear exit before the loan comes due.

Those costs are meaningful. A borrower who uses private lending on a long-term hold where conventional financing was available is leaving money on the table. A borrower who uses private lending to close a time-sensitive acquisition, execute a value-add strategy, and refinance at stabilization is using the tool exactly as designed.

The Types of Loans Private Lenders Make

Private lending is not one product. It is a category, and the lenders within it have specialized into distinct product types with different underwriting standards, terms, and use cases.

Bridge Loans

Short-term transitional financing used to bridge between stages of a deal: acquisition before renovation begins, stabilization before permanent financing, or a purchase before a replacement property closes. Bridge loans are typically 6 to 24 months, structured as interest-only, with the full principal due at maturity.

Fix-and-Flip Loans

A specific type of bridge loan designed for acquisitions that will be renovated and sold. The lender underwrites to ARV rather than current value, since the property's post-renovation worth is the basis for the exit. Terms are typically 6 to 18 months. Draw schedules release renovation capital in stages tied to completion milestones.

DSCR Rental Loans

Long-term financing for stabilized rental properties, underwritten on the property's debt-service coverage ratio rather than the borrower's personal income. If the property cash-flows above a threshold, typically 1.0x to 1.25x DSCR, the loan qualifies. Volume in this product category grew 94 percent year-over-year through November 2025, according to HousingWire, tracking 42 originators across 29,066 closed loans.

New Construction Loans

Ground-up construction financing, disbursed in draws against a budget as work progresses. These loans carry more complexity than rehab financing because the asset does not yet exist, which means underwriting is based on projected value and the borrower's ability to execute the build. LTC is the primary underwriting metric.

Commercial Bridge Loans

Short-term financing for commercial and multifamily properties, typically with higher minimum loan sizes ($1 million or above) and different underwriting criteria reflecting the income-producing nature of the asset. Lenders in this segment often specialize by property type.

Who Uses Private Lending, and Why

The borrower profile in private lending is broader than most people expect.

Fix-and-flip investors are the most visible segment. They depend on private lending because conventional financing cannot accommodate the speed or the property condition requirements of their model. A property that needs $80,000 in renovation to reach value does not qualify for a bank loan. Private lending exists to fund the gap between acquisition and stabilization.

Rental portfolio builders use DSCR financing to scale acquisitions without hitting the personal income ceilings that limit conventional borrowing. As a portfolio grows, the properties themselves qualify for financing rather than the investor's W-2.

Developers use construction and bridge loans to finance ground-up builds and acquisitions at stages where permanent financing is not yet available. The private loan carries the deal until the project reaches a stabilization point where long-term capital makes sense.

Experienced investors often use private lending even when conventional financing is available. The reason is certainty of close. A private lender who commits to funding a deal delivers on that commitment in a predictable timeline. Banks can retrade terms, extend timelines, or decline at the last minute based on conditions that have nothing to do with the deal itself.

Private lending is not a lender of last resort. It is a tool optimized for speed, flexibility, and deals that do not fit the conventional mold.

How Private Lenders Make Underwriting Decisions

The underwriting framework in private lending centers on the asset, but experienced lenders look at more than a single ratio.

The property's current value establishes the baseline. For value-add deals, the after-repair value is the relevant figure, and lenders typically discount ARV assumptions conservatively. A lender will scrutinize the rehab budget and the comparables supporting the projected value. Overstated ARVs are the most common source of loan losses.

Exit strategy is the second critical variable. How does the borrower plan to repay the loan? A sale requires a functioning resale market and a realistic timeline. A refinance requires that permanent financing will be available when the term expires. Lenders without a clear exit path decline the deal or price the uncertainty into the rate.

Borrower experience matters, particularly on complex projects. A first-time flipper taking on a full gut renovation is a different risk profile than a borrower with twenty completed projects. Lenders factor this into both approval decisions and leverage. A strong track record can unlock higher loan amounts relative to cost.

Liquidity is also evaluated. Borrowers who do not have reserves to cover holding costs or cost overruns introduce execution risk that the lender absorbs. Most private lenders require some evidence that the borrower can sustain the project if something goes sideways.

Running that underwriting process efficiently, across a pipeline of deals, is where private lending operations either scale or stall. The lenders who grow are the ones who have systematized origination, underwriting, draw management, and servicing. That operational infrastructure is what separates a real lending business from a lender doing a handful of deals a year.

Why Private Lending Has Grown Into a Mainstream Market

The private lending industry's growth traces directly to the 2008 financial crisis and the regulatory response that followed.

The Dodd-Frank Act, Basel III capital requirements, and the regional bank failures of subsequent years all constrained traditional bank lending for real estate investment. Banks pulled back from bridge loans, construction financing, and non-owner-occupied properties that carried higher regulatory capital weights. The gap they left was substantial.

Private lenders filled it. Capital that had previously been deployed in other asset classes moved into real estate debt, attracted by yields that consistently outperformed public credit markets. Data cited by Lenderkit suggests direct lending returned an average of approximately 11.6 percent annually over the 2008 to 2023 period, compared to 5 percent for leveraged loans and 6.8 percent for high-yield bonds.

The result was an industry that grew from a niche alternative into a core component of real estate finance. The US private lending market logged approximately 276,900 loan originations in 2024, growing at roughly 14 percent year-over-year according to Forecasa. The DSCR product alone, which barely existed ten years ago, logged over 29,000 originations across a sample of 42 lenders in a single year.

That scale has brought professionalization. The private lending market today looks fundamentally different from the hard money shops of twenty years ago. Lenders run on loan origination software, service portfolios across hundreds of borrowers, manage capital from institutional investors, and operate with compliance structures that would have been unrecognizable in the industry's early days.

The opportunity is real. So are the operational demands.

Frequently Asked Questions

What is the difference between private lending and hard money lending?

The terms are often used interchangeably, and increasingly that usage is accurate. Historically, "hard money" referred to asset-based loans from professional companies focused primarily on collateral, while "private money" referred to capital from individuals operating on a relationship basis. The line between those two categories has blurred significantly as the industry has matured. The National Private Lenders Association formally encouraged the industry to retire the "hard money" label in 2022, replacing it with "private lending," "bridge lending," and "transitional lending." Most professional lenders today use private lending as the umbrella term.

What interest rates do private lenders charge?

Rates vary by product type. Bridge and fix-and-flip loans typically run in the 9 to 13 percent range in the current environment, reflecting short terms and construction risk. DSCR rental loans for stabilized properties generally fall in the 7 to 9 percent range. Origination fees of 1.5 to 3 points are standard in addition to the interest rate. Specific rates depend on loan type, property type, leverage, and borrower experience.

Is private lending regulated?

Yes, though differently than bank lending. Private lenders must comply with state usury laws capping the interest rates they can charge. Depending on volume and loan type, state licensing requirements may apply. Because most private lending is for investment or business purposes rather than owner-occupied residential, many of the consumer protection regulations that govern conventional mortgage lending, including Dodd-Frank's ability-to-repay rules, do not apply. Lenders should verify the regulatory requirements in each state where they operate.

How do I qualify for a private loan?

Qualification in private lending centers on the deal rather than the borrower's financial profile. Lenders evaluate the property value or ARV, the LTV ratio, the exit strategy, and the borrower's experience and liquidity. Strong credit scores are not required, but evidence that the project can be executed and the loan repaid is. A clear scope of work, realistic comparables, and reserves to cover holding costs improve the likelihood of approval.

Can anyone become a private lender?

Technically yes. An individual with capital can lend money secured by real estate. In practice, operating a private lending business at any real scale requires origination infrastructure, underwriting capacity, servicing systems, and compliance oversight. Individuals deploying personal capital into one-off deals operate differently from lending companies managing a portfolio of dozens or hundreds of loans. The regulatory picture also varies: some states require licensing above a certain loan volume, and business-purpose lending carries its own compliance considerations.

Baseline is built for private lenders who have moved past the one-deal-at-a-time stage. From origination through servicing and capital management, the platform handles the operational complexity so lenders can focus on deals. See how it works at baselinesoftware.com/contact-us