President Trump's recent announcement to ban large institutional investors from purchasing single-family rental (SFR) properties came as a shock to many in the real estate investment community. While the policy aims to increase homeownership opportunities for American families, it presents a significant opportunity for private lenders who specialize in serving smaller investors.

The Policy Shift

The ban, announced on January 7, 2026, through his Truth Social account, targets large institutional investors who have been accumulating SFR properties at scale over the past decade. Some notable institutional investors include Blackstone, American Homes 4 Rent, Progress Residential, and Pretium Partners. Trump framed the policy as a response to housing affordability concerns, arguing that institutional ownership has pushed home prices beyond the reach of ordinary Americans seeking homeownership.

A Fragmented Market Creates Opportunity

One of the most significant implications of the institutional ban is the fragmentation it will create in SFR ownership, particularly in markets like Atlanta, Charlotte, and Phoenix, where institutional ownership is most concentrated. Rather than large, well-capitalized institutions controlling thousands of properties through centralized operations, the market will shift toward a more dispersed ownership structure dominated by individual investors and smaller operators.

The fragmentation of ownership is precisely where private lenders stand to benefit. Unlike their institutional counterparts who finance large, single-borrower portfolios, private lenders have built their business models around serving mom-and-pop operators and small to medium-sized investors. These borrowers typically own anywhere from a handful to a few dozen properties and require more flexible, relationship-based financing that traditional banks and institutional lenders often cannot or will not provide.

The Deal Flow Equation

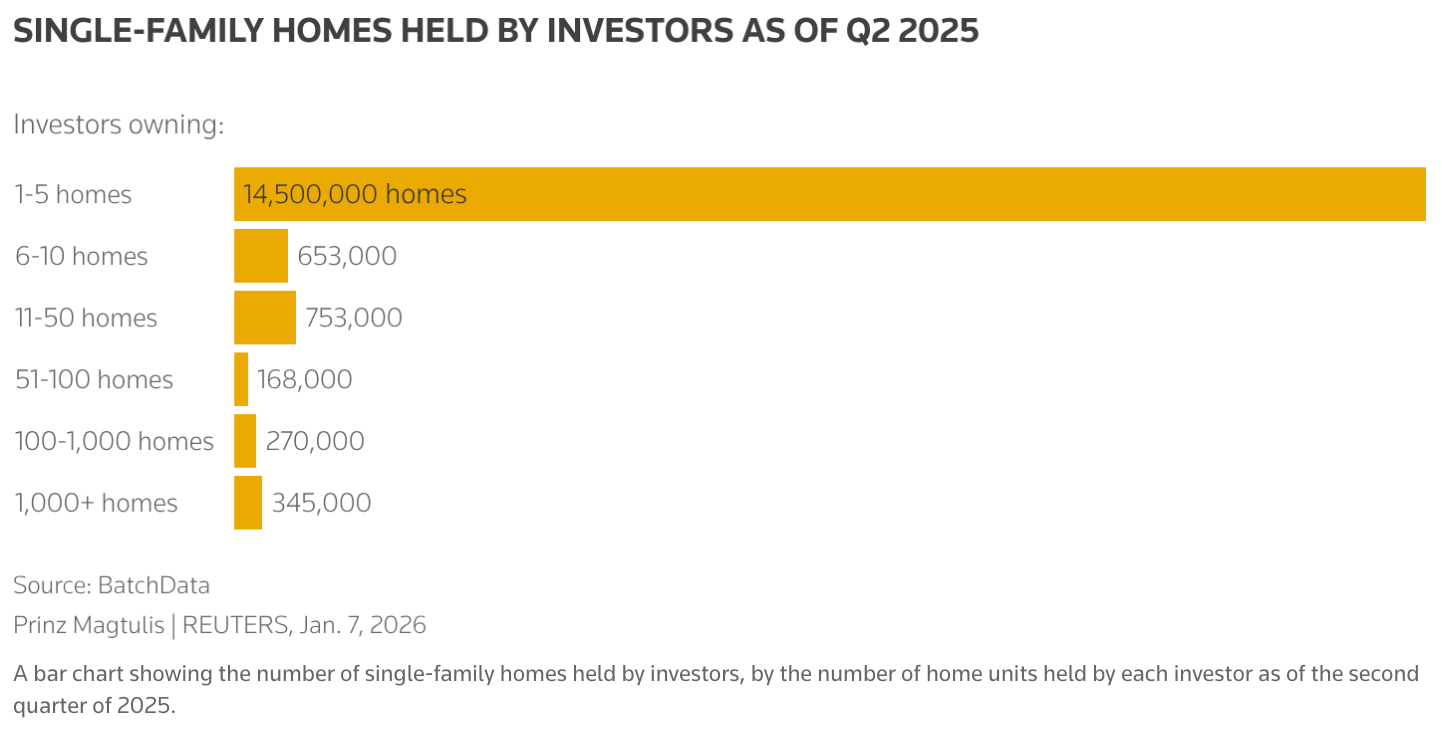

If the same number of properties must be financed but are now spread across many more buyers and owners rather than concentrated in institutional portfolios, private lenders will see a substantial increase in deal flow. According to Reuters, institutional ownership of single-family properties represents approximately 3% or so of the roughly 16 million SFRs owned as investments in the US, a relatively small percentage of all investment properties nationwide.

This still translates into 615,000 SFR properties owned by investors with 100+ SFRs in their portfolio. With a fraction of these homes changing hands and going through financing events each year, it could result in tens of thousands of additional transactions for private lenders to finance each year. Each small investor acquiring one to ten properties represents a potential financing opportunity, whereas previously those same properties might have been rolled into a single institutional acquisition financed through large-scale debt facilities.

Private lenders are uniquely positioned to capitalize on this shift. They understand the nuances of working with smaller investors who may have less sophisticated financial profiles than institutions but bring local market knowledge, sweat equity, and long-term commitment to property management. The underwriting criteria, loan structures, and relationship dynamics that private lenders have perfected over years of serving this market segment will become even more valuable as this borrower base expands.

Furthermore, small and medium-sized investors often require different types of financing throughout their investment lifecycle, including residential transition loans (RTL), bridge loans, and debt service coverage ratio (DSCR) loans. This creates multiple touchpoints and revenue opportunities for private lenders with each borrower relationship.

The Price Floor Problem

The ban is not without potential consequences on the broader housing market, and with implications for private lenders as well. One significant concern is that removing institutional buyers eliminates the price floor created by institutional buyers, which has supported housing values. Institutions purchasing SFRs for yield have been reliable bidders in markets across the country, particularly in Sunbelt metros where rental demand is strong and cap rates remain attractive.

When institutional capital flows into single-family homes, it provides consistent demand and pricing support, especially during market downturns. These large buyers have been less sensitive to short-term market fluctuations, focused instead on long-term yield and portfolio diversification. Their presence created consistent demand and established valuation baselines, especially during market downturns when individual buyers might retreat. When markets softened, institutions with substantial capital reserves could continue acquiring properties, preventing prices from falling as steeply as they might otherwise.

For private lenders, this volatility is a double edged sword. On one hand, the collateral underpinning their loans may be subject to greater fluctuation, potentially increasing credit risk in their portfolio. Conversely, market dislocations and price corrections often create attractive buying opportunities for nimble investors, which can drive increased lending activity. Private lenders with strong underwriting discipline should be able to navigate this environment, but the loss of the institutional price floor will inevitably increase default risk.

New Channels for Institutional Capital

The ban doesn’t necessarily mean institutional capital will completely abandon the SFR asset class. Institutions can redirect that capital and still participate in the asset class through private credit vehicles. Rather than buying homes directly, institutions can deploy capital through structured credit facilities that fund smaller operators, with private lenders serving as the origination and servicing layer.

We’re already seeing this model take shape in the private lending industry, where institutions have partnered with large originators to provide warehouse lines, securitization takeout, or direct loan participation.

This model offers several advantages. Institutions can maintain exposure to the SFR asset class and its yields while reducing the operational complexity of property management. Private lenders gain access to larger, more stable capital sources to fund their lending operations, potentially at better terms than they could achieve independently. And small investors get access to financing that, while originated by private lenders they know and trust, is ultimately backed by institutional capital.

In essence, the market may expand and further evolve toward a structure where institutional capital sits one level removed from property ownership, flowing through private credit channels and origination platforms rather than through direct acquisition. This creates a larger role for private lenders as essential infrastructure in the capital formation value chain.

It’s also worth noting that institutions have been net sellers of their SFR portfolios over the last several years. According to a recent article from SFR Analytics, large institutional SFR buyers have largely stopped buying homes over the past three years. In fact, they have been net sellers since interest rates began rising in 2022. The ban could accelerate their disposition strategy and create an influx of cash that needs to be deployed.

Strategic Positioning for Private Lenders

Trump’s ban on institutional ownership of single-family homes is ultimately a policy designed to prioritize individual homeownership and reduce the influence of large investors on housing affordability. Whether it achieves these goals remains to be seen, and much will depend on implementation details, enforcement mechanisms, and potential legal challenges.

For private lenders, however, a more fragmented ownership structure in the single-family rental market creates more transactions, and more opportunities to deploy capital, especially in markets with heavy concentration of institutional ownership. The challenge will be navigating the potential price volatility in the absence of a price floor.

As the market adapts to the new paradigm, private lenders who can efficiently provide loans to smaller investors, while potentially partnering with institutional capital sources, will be best positioned to capture the newly created market share.